With Andy Thurai, VP & Principal Analyst, Constellation Research

The AI gold rush is on. The paths to monetization are seemingly endless but the most obvious converge on making humans more productive or supercharging existing business models like search advertising or subscription licenses. Much of AI adoption in enterprise IT is hidden. Our research shows a very high overlap (around 40-60%) between AI adoption in enterprise tech and embedded AI inside software from the likes of Salesforce, ServiceNow, Workday, SAP, Oracle and other major players. But the rapid advancements of tools from AI leaders and an emerging group of independent firms is causing customers to think differently. Catalyzed by the OpenAI Microsoft partnership, organizations are rapidly trying to figure out how to apply these tools to create competitive advantage. Every firm on the planet wants to ride the AI wave. Virtually overnight, investment capital has shifted to fund early stage AI startups with much less funding required relative to previous boom cycles.

In this Breaking Analysis we review ETR data to quantify the state of AI spending in the enterprise and look at the positions of several key players in the space that offer AI tools and platforms. To do so we invite Andy Thurai, CUBE contributor, VP and principal analyst at Constellation Research. Andy will help us unpack the hits and misses from this past week’s Google IO conference and give us his perspectives on what it takes to catch the AI wave and avoid becoming driftwood.

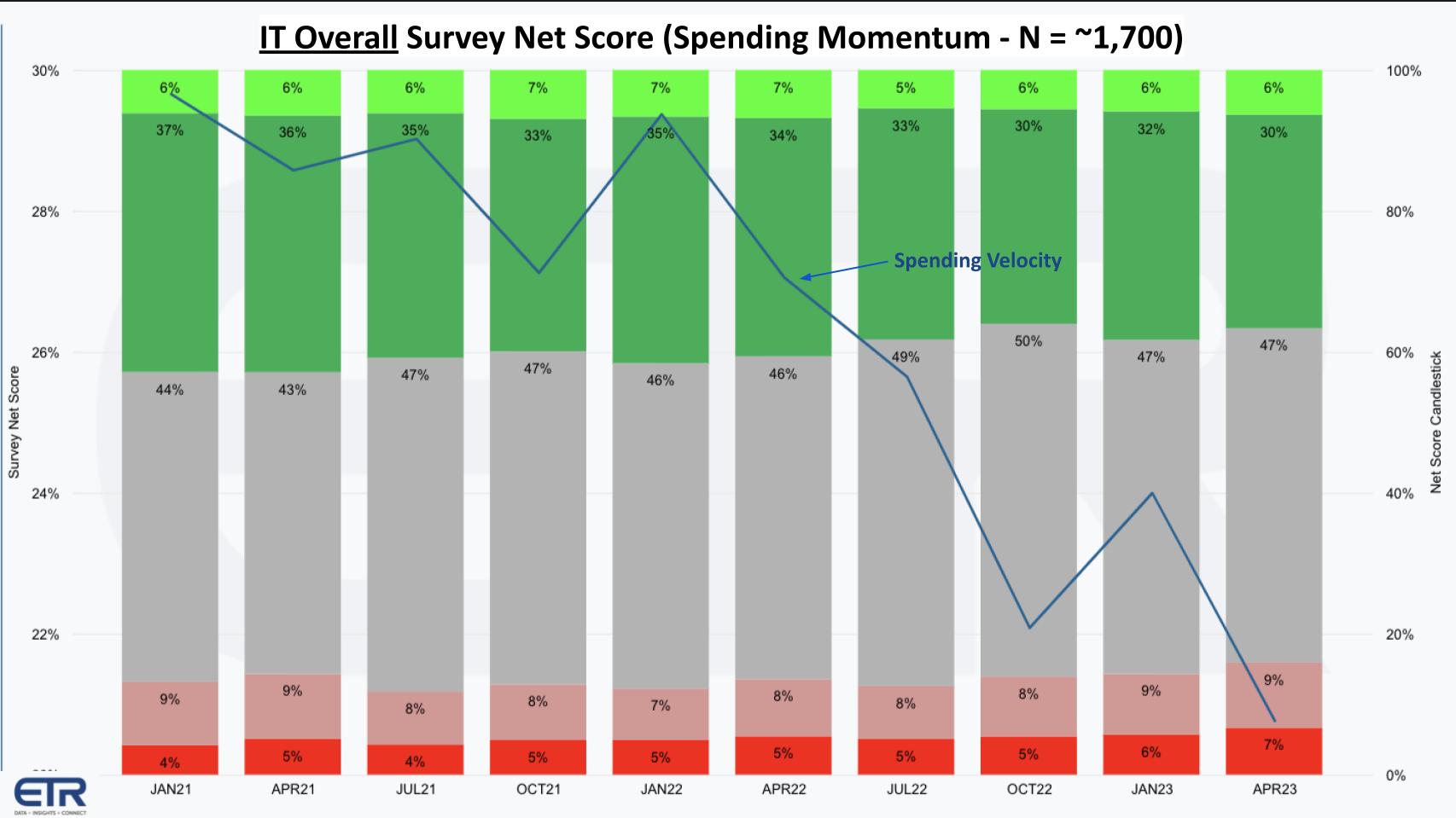

First, the Macro IT Spending Climate

The chart above shows ETR survey data going back to January 2021. The survey reaches nearly 1,700 IT decision makers each quarter. The chart shows the breakdown of spending across five categories. The lime green bars show the percent of customers adding new platforms. The forest green shows the percent spending 6% or more relative to previous years. The gray bars depict flat spend. The pinkish area is spending down 6% or worse; and the bright red is the percentage of customers retiring platforms. Subtract the reds from the greens and you get Net Score which measures overall spending momentum, shown on the blue line. The trend couldn’t be more clear. You can see coming into 2022 there was optimism that deteriorated throughout last year. And while the entry into 2023 brought an upbeat outlook, interest rates and earnings revisions have put a pin in that enthusiasm and the trend line has continued to decline.

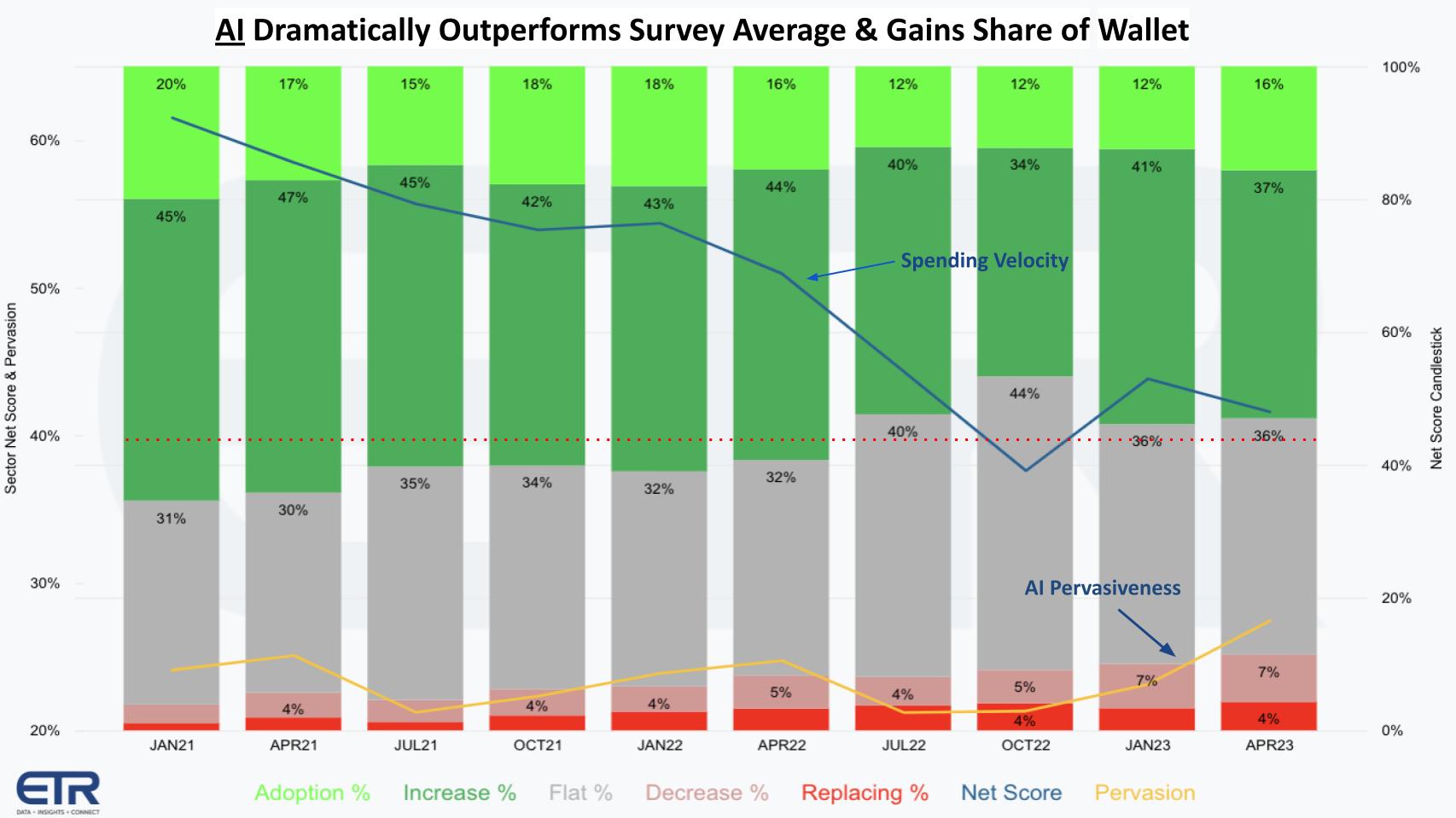

Spending on AI is on a Different Trajectory

Below we take a look at the data for AI using the same methodology.

The difference is obvious as the pace of decline on the blue line is less steep. The other notable point is the blue line has consistently stayed about the 40% mark shown by that red dotted line. The 40% mark represents highly elevated spending momentum. In context, spending momentum in AI is 22 percentage points higher than enterprise tech spending overall.

The yellow line represents the pervasiveness of AI in the data set. This is a measure of AI’s relative share of the total survey. You can see peaked in the April 22 survey, then declined last summer but since the launch of ChatGPT it is steadily increasing and reaching new highs.

Andy Thurai’s commentary on this data is summarized as follows:

There has been a significant increase in the adoption of AI in recent years, and he attributes this to two factors:

- The success of ChatGPT, a large language model developed by OpenAI and Microsoft. ChatGPT has been used in a variety of successful proof-of-concepts, and it has helped to demonstrate the potential of AI to improve business processes.

- The desire of enterprises to reduce costs. AI can be used to automate tasks, improve efficiency, write code and reduce errors. This can lead to significant cost savings for enterprises.

The key point is while overall spending on IT is decreasing, the spending on AI is now increasing as enterprises look for ways to offset the cost of AI by reducing spending in other areas.

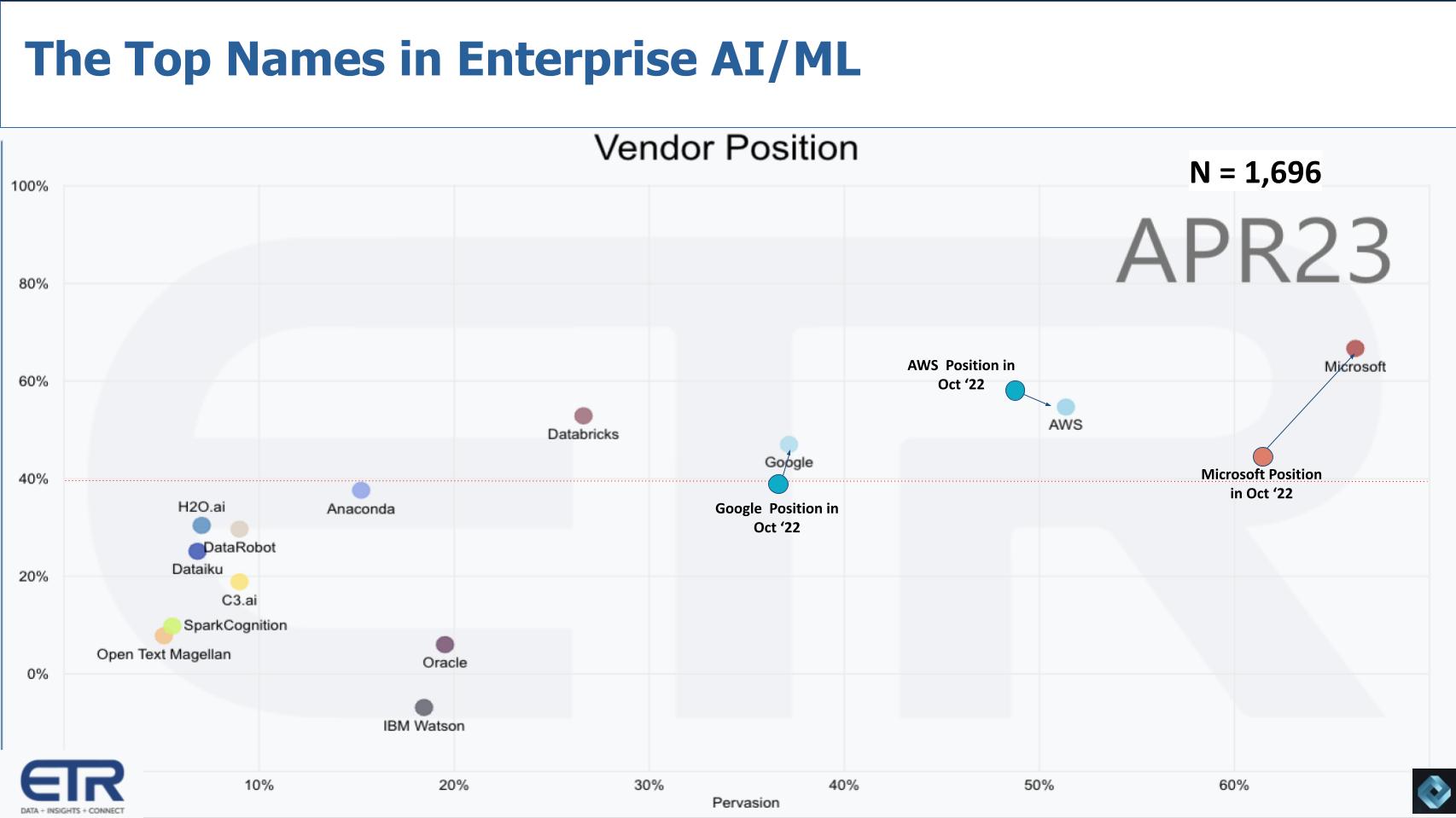

AI Leadership & the Microsoft OpenAI Tailwind

The chart above shows ETR survey date of nearly 1,700 IT decision makers from the April survey. The vertical axis is Net Score or spending momentum. The red dotted line at 40% indicates highly elevated spending velocity. The horizontal axis is pervasiveness in the data set. The following points are noteworthy in the data:

- The big 3 hyperscalers are dominating along with Databricks, which as we’ve reported has very strong market momentum;

- Microsoft’s position since the OpenAI partnership has escalated dramatically relative to the other leaders.

Anaconda is a popular distro of Python, R and other tools for data scientists. And you can see there’s a pack of companies including H2O.ai, DataRobot, Dataiku and some others we’ll talk about in a moment. As well, both Oracle and IBM Watson show up in the ETR data as essentially AI offerings going into captive products within the respective installed bases of those companies.

Andy Thurai’s puts and takes on this data can be summarized as follows:

- Microsoft experienced a phenomenal jump in market share due to ChatGPT hype, significantly outperforming its competitors.

- Satya Nadella, Microsoft’s CEO, discussed the new AI wave solution during the Q3 earnings call, highlighting the company’s aim to bring AI workloads to Microsoft Cloud.

- Nadella also mentioned Microsoft’s powerful AI infrastructure and encouraged users to train their own large models on it.

- Despite the hype, Microsoft’s OpenAI currently has only 2,500 customers, while Azure Arc, a hybrid management, deployment security solution, boasts 15,000 customers. The point is Microsoft is barely scratching the surface.

- Microsoft is using AI technologies, such as Cosmos DB, to position itself as the go-to option for AI solutions.

- Surprisingly, Microsoft’s primary goal isn’t just capturing AI workloads, but rather making a dent in Google’s search business. By developing an AI-powered search, the company hopes to seize a portion of the highly profitable search advertising market.

The discussion with Thurai highlights how ChatGPT is changing the landscape of technology, with Microsoft leveraging AI’s potential to challenge Google’s dominance in the search market. That was a key vector of Microsoft’s original strategy. But more relevant to enterprise IT, Microsoft and OpenAI have catalyzed responses from not only Google but also AWS and numerous other players.

[Listen to Andy Thurai’s commentary about the AI horses on the track].

Digging into Some of the Larger AI Players

Why Did IBM Watson Fail?

A stunning moment occurred in 2011 when IBM Watson beat Ken Jennings, the greatest Jeopardy player of all time. At the time we were impressed at this amazing demonstration. Many deep AI experts poo poo’d the technological milestone while others eventually even went so far as to call out Watson as fraudulent. The fact remains, however that IBM was way ahead of the mindshare curve. It most certainly had the technological and financial resources to take Watson to the next level and apply AI in new and exciting ways. Our view is IBM turned Watson into a high value and complicated services engagement and failed to envision how to apply the technology to solve everyday problems for users at scale.

[Watch the clip of Watson’s milestone of machine beating human at Jeopardy].

We asked Andy Thurai why IBM Watson failed and where it goes from here.

His key points from the discussion include:

- IBM, despite being a strong research company, has faced challenges in figuring out the best ways to bring its AI innovations to market.

- IBM faced limitations in technology, usability, and the absence of a mature AI-related regulatory environment, which contributed to IBM’s slow progress in the AI space.

- IBM is now working to catch up by launching offerings like AI Studio, Data Store, Governance, etc.

- Two standout features of IBM’s AI strategy include:

- A Center of Excellence with over a thousand AI experts who can work closely with customers to offer guidance and support.

- An Environmental Intelligence Suite that provides information on the carbon footprint of training AI models, catering to environmentally-conscious companies.

Despite these efforts, IBM still has a long way to go in catching up with competitors in the AI market. However, their unique offerings and expertise could help the company gain traction and win over customers in the long run.

Microsoft has Changed the Game but has it Changed the Trajectory of Bing?

We’ve said a number of times on theCUBE that Microsoft went from third place in AI technology relative to Google and Amazon and then all of a sudden cut the line with the OpenAI deal. It became #1 overnight from a business model and awareness standpoint. And Satya Nadella has touted a cheshire cat-like grin in terms of going after Google’s search business.

But as reported in The Information, Microsoft wants to bid to embed Bing into Firefox. Microsoft will pay a ton of money for that right but it’s a clear sign that BingGPT has failed to significantly move the needle in search.

Thurai’s comments in this regard are that right now, in his view, for Microsoft it’s all about disrupting Google’s search business. Here’s a summary of his thoughts:

The immediate focus for companies like Microsoft is not solely on AI workloads, but rather on the lucrative search advertising market. Key points Thurai makes include:

- AI workloads are seen as a long-term opportunity, with their full potential expected to be realized over decades.

- Microsoft aims to revive its search business, including Bing, by integrating AI solutions like ChatGPT.

- However, Google has either caught up or surpassed Microsoft in terms of AI integration in search, making it a highly competitive race between the two tech giants.

This will be an ongoing battle between Microsoft and Google in the AI and search domains, with both companies trying to innovate and outperform each other. Which leaves an interesting opportunity possibly for AWS to emerge as the leader in enterprise AI.

Google Flexes its AI Muscles at IO

Google showered us with a firehose of announcements at Google IO. Andy Thurai wrote a piece on focusing on Google’s hits and misses. The strongest parts of the announcements in our view were the integration of AI into Google Workspace and its Gmail to help write. In addition the photo editing we’ve seen before has been enhanced and Google improved and uplifted its Bard capabilities in a really impressive show of AI force. Comparing Bard and ChatGPT is an interesting exercise with each platform showing strengths and weaknesses.

Thurai’s post also highlighted what he thought were some misses as well. He didn’t think Google’s coding helper went far enough and he said he was disappointed with the limited focus on industry breadth, even though they had cited tools for medical. In addition Thurai wasn’t overly impressed with the GCP announcements and integration.

Key points from the conversation with Thurai around Google’s announcements include:

- Google has introduced AI-enabled cognitive search, which has the potential to be a game-changer and snatch market share back from Microsoft.

- Unlike ChatGPT, which relies on older, pre-trained models, Google claims to offer real-time cognitive search for more accurate and relevant results.

- Google also presents a mix of synthesized search results (similar to ChatGPT) and regular search results, catering to different user preferences.

- These advancements could extend beyond search and have applications in e-commerce, allowing users to search for images and other content to build online stores, something not currently possible with ChatGPT.

- Additional innovations include Google Workspace, photo image editing, and multiple language models.

The discussion with Thurai highlights Google’s aggressive efforts to maintain its dominance in the search market and expand its AI capabilities to outperform competitors like Microsoft.

[Watch and listen to Andy Thurai’s comments on Google’s AI announcements at its recent IO event].

AWS’ Building Block Approach

Let’s talk about AWS’ lego block approach. AWS targets developers and enterprises, which both Google with GCP and Microsoft Azure do as well. But AWS is not focused on disrupting Google search, rather it wants to provide building block elements to enable AI. Microsoft and Google have other consumer and advertising aspirations, whereas AWS does not, notwithstanding Amazon has Alexa.

AWS’ large language model announcements last month underscored this approach and customer interest has been off the charts. Our conversations with various sources indicate that an overwhelming percentage of inbound sales inquires to AWS involve discussions around Bedrock, Titan, CodeWhisperer and new silicon to support the application of large language models. As well, AWS has partnered with companies like Hugging Face and others to extend the offerings from ecosystem partners. Recently John Furrier interviewed execs from AWS, Hugging Face and AI21 Labs to discuss industry trends and the overall market.

Andy Thurai’s take on AWS’ offerings are summarized as follows:

The discussion centered on Amazon’s approach to AI, which, as mentioned, involves providing building blocks for users and continually iterating their offerings due to increasing competition. Other key points from the conversation include:

- Amazon provides foundational models for text, images, and other content through APIs, with options like Anthropic, AI21 Labs, Stability AI, and Amazon’s own Titan.

- AWS claims to offer the ability to privately customize models using an organization’s own data, which could be a differentiator in the market, although it’s likely others will follow suit.

- Amazon CodeWhisperer is a good start but not yet on par with more established tools like CodePilot.

- The partnership with Hugging Face is viewed as a significant move, providing users with more options for accessing models.

- Amazon has also been developing customized infrastructure for AI, such as Trainium-based models for training and Inferentia-based models for inference.

Overall, Amazon’s strategy of providing versatile, customizable AI solutions and partnerships to stay competitive in the rapidly evolving market is a strong approach and will likely allow Amazon to maintain its AI leadership amongst its core customers.

[Listen and watch Andy Thurai’s take on AWS’ recent announcements around foundation models].

What about Oracle?

Oracle, like IBM, will focus mainly if not exclusively on improving its own stack and will narrowly appeal to a captive installed base. Oracle has been infusing AI into its database products for years as part of its autonomous database initiative to automate rote tasks of database administrators. While we don’t expect Oracle to lead with AI innovation relative to hyperscale cloud players, it will continue to lead in mission critical workloads and follow industry trends in terms of applying AI to its databases and enterprise software offerings.

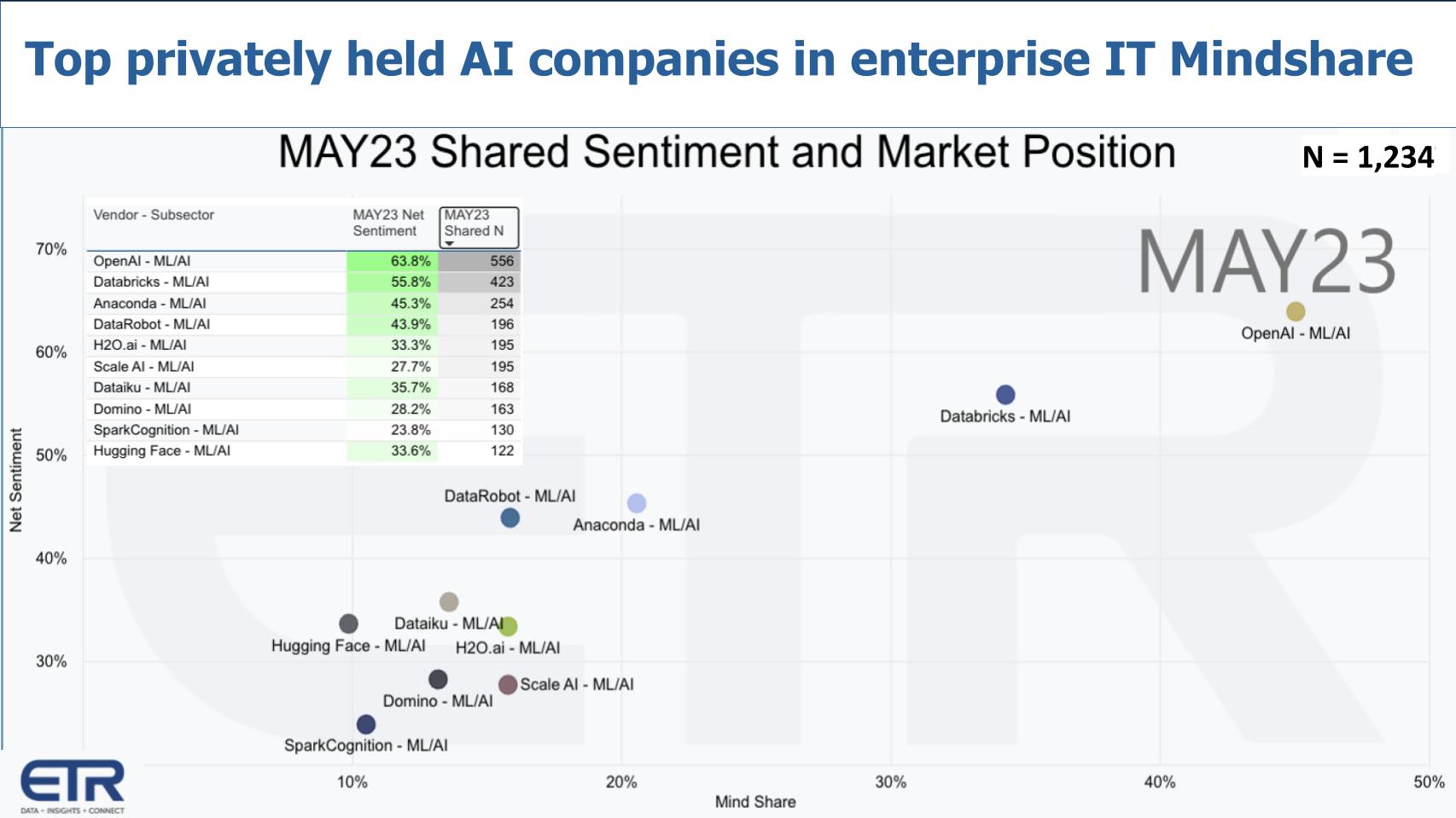

The Top 10 Privately Held Companies in Enterprise AI

The ETR Emerging Technology Survey (ETS) is a quarterly survey of more than 1,200 IT decision makers focused exclusively on non-public companies. The survey measures Net Sentiment (i.e. intent to engage) and Mindshare (i.e. awareness). The chart below filters the top 10 companies in ETR’s ETS ML/AI taxonomy based on Mindshare.

Note that OpenAI wasn’t even in the data until last fall and then and now have the #1 position on both dimensions. Databricks is prominent with its ML/AI tool chain but also some of its other products may be seeping into the sector. But they also show up in the database/data warehouse section so this is intended to be AI only. You can see the other emerging companies like Anaconda, which is a platform for data science, DataRobot, Dataiku…and Hugging face which we’ve previously discussed. Hugging Face has announced partnerships with AWS and more recently with IBM and others.

We asked Andy Thurai to share his thoughts on this data and if there were any surprises. While the momentum of OpenAI was no surprise, he did feel that Hugging Face was underrepresented in the survey, despite what we would observe as pretty solid momentum and presence. Further, summarizing Thurai’s comments:

Thurai felt Hugging Face had a relatively low rating and he highlighted its significant presence in the AI landscape. Key points include:

- Hugging Face has been “all over the place” in a good way, forming relationships with major tech companies like Azure, Amazon, IBM, and Google.

- The company has become the de facto model repository for AI, providing a platform for data scientists to share and train their models.

- He is also believes Hugging Face is well-positioned when considering its well-known status in the realms of model management, training, and repository.

In summary, Hugging Face’s widespread partnerships and critical role in the AI community as a central hub for AI models put it in a good position and we would expect continued improvement in the ETR ETS survey over time.

[Watch and listen to Andy Thurai’s surprises on the emergent AI company data].

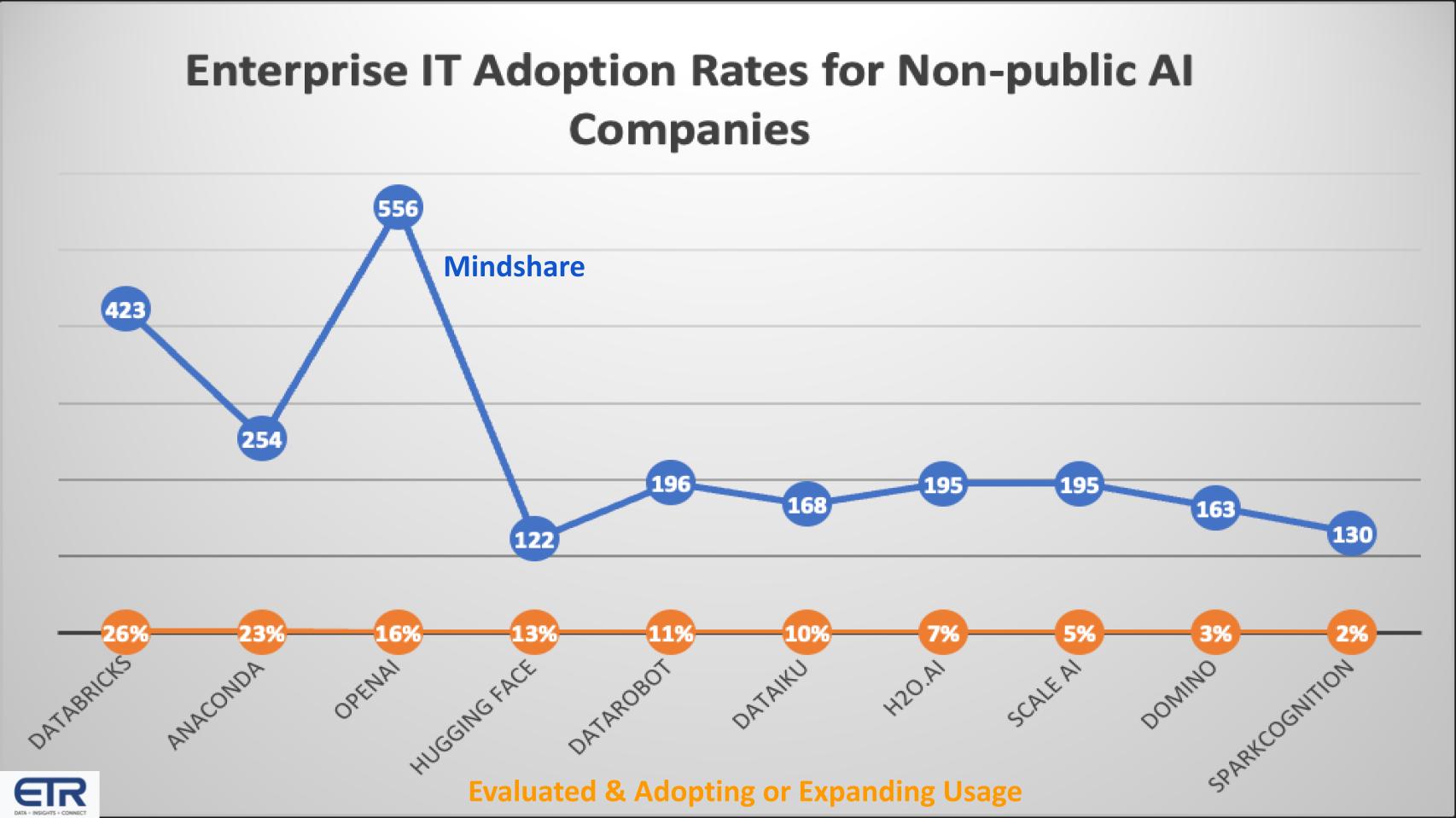

AI Mindshare is One Thing…Adoption is Everything

It’s great to have mindshare but to really get ROI you have to have adoption and show real business value. This next data chart aims to measure just that.

The data above plots the mind share data we showed earlier on the blue line and the percent of those customers familiar with the AI platform that have evaluated the platform and intend to use it or expand its usage. So the orange data measures adoption. Databricks has the highest adoption rate at 26% followed by Anaconda, then OpenAI at 13% – everyone is using ChatGPT personally but what about adoption in the enterprise? Then Hugging Face at 13%, DataRobot and Dataiku in the low double digits, followed by Scale AI, Domino and SparkCognition.

[Andy Thurai comments on the ETR adoption data].

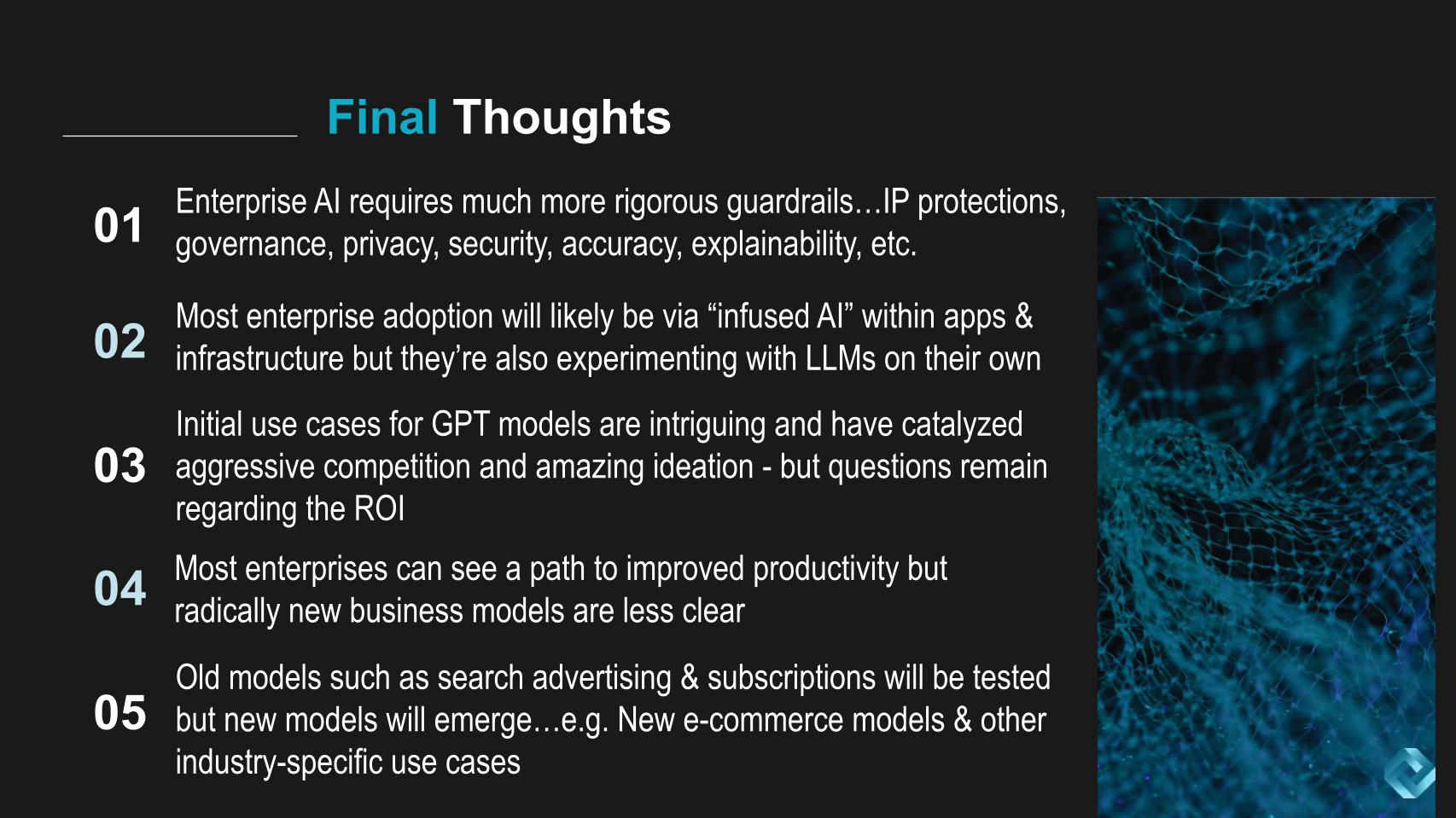

What to Watch in Enterprise AI Going Forward

Enterprise AI is a different animal…IT needs rigorous guard rails they’re concerned about IP leakage, they want super strong governance, privacy, security, transparency, explainability, bias controls, etc. And the second point below is most enterprises won’t build AI, rather they’ll buy it as embedded within their enterprise apps and their AI powered infrastructure. Having said that, they’re all experimenting with AI in new ways thanks to ChatGPT to see how they can create unique competitive advantage.

Last time Andy came on Breaking Analysis in December of 2022 we said AI goes mainstream but the ROI remains elusive and we think that was an accurate take. ChatGPT is intriguing. It’s game-changing and has kicked off responses from all sorts of competitors. Of course we’re seeing AI-washing everywhere. We’ve seen other responses like Google’s “Code Red,” IBM re-thinking Watson, AWS getting to market, everyone announcing AI, including theCUBE. We built theCUBE AI demo very quickly for not a lot of money and it appears to be extremely useful.

The point is everyone is still trying to figure out the ROI and the right business model. It’s pretty clear people see a path to better productivity with humans in the loop but radical business models are not as clear. We’ll pave the cowpath in search ads and subscription license models but we should expect new models to emerge. It’s not clear today what those models look like.

One that we’ve envisioned is a disruptive e-commerce model that goes after Amazon’s massive warehouse infrastructure, which has been a competitive advantage. What if Google GPT enables better shopping and direct shipping from the manufacturer, more along the lines of what Alibaba does… and what about industry-specific use cases and business models that could emerge? Something new will come out of this that will surprise a lot of people.

Below are Andy Thurai’s final thoughts.

The urgency to integrate AI into applications to improve efficiency and productivity must be heightened. At the same time there are several the challenges and responsibilities that come with that, including:

- Integrating AI into applications can enhance efficiency, but vendors and users need to assume responsibility and liability for potential issues of bias, privacy and data quality.

- Enterprises need to consider governance, security, ethical, and responsibility aspects when incorporating AI, with CEOs and CIOs thinking about potential risks.

- To effectively implement AI, businesses should start with a use case, focusing on the problems they want to solve and working backwards to build rigor, governance, and controls.

- AI can be applied in various areas, such as IT operations, AI ops, service ticket companies, and infrastructure optimization, to improve efficiency and minimize costly downtime.

In summary, we believe businesses must approach AI integration with a focus on specific use cases, building proper governance and controls to ensure responsible and effective AI adoption.

On the one hand, tapping into AI has suddenly become easy. Figuring out how and where to apply it to your business safely however is not so trivial.

As always, we’d love to know what you think and where you’re applying AI to improve business results.

Keep in Touch

Many thanks to Andy Thurai for his insights and participating in this Breaking Analysis segment. Alex Myerson and Ken Shifman on production, podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight who help us keep our community informed and get the word out. And to Rob Hof, our EiC at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.