Is the glass half full or half empty? Well, it depends on how you want to look at it. CIOs are tapping the brakes on spending that’s clear. The latest macro survey from ETR quantifies what we already know to be true, that IT spend is decelerating. CIOs and IT buyers forecast that their tech spend will grow by 5.5% this year, a meaningful deceleration from their year end 2021 expectations…but these levels are still well above historical norms – so while the feel good factor may be in some jeopardy, overall things are pretty good – at least for now.

In this Breaking Analysis, we update you on the latest macro tech spending data from Enterprise Technology Research, including strategies organizations are employing to cut costs…and which project categories continue to see the most traction.

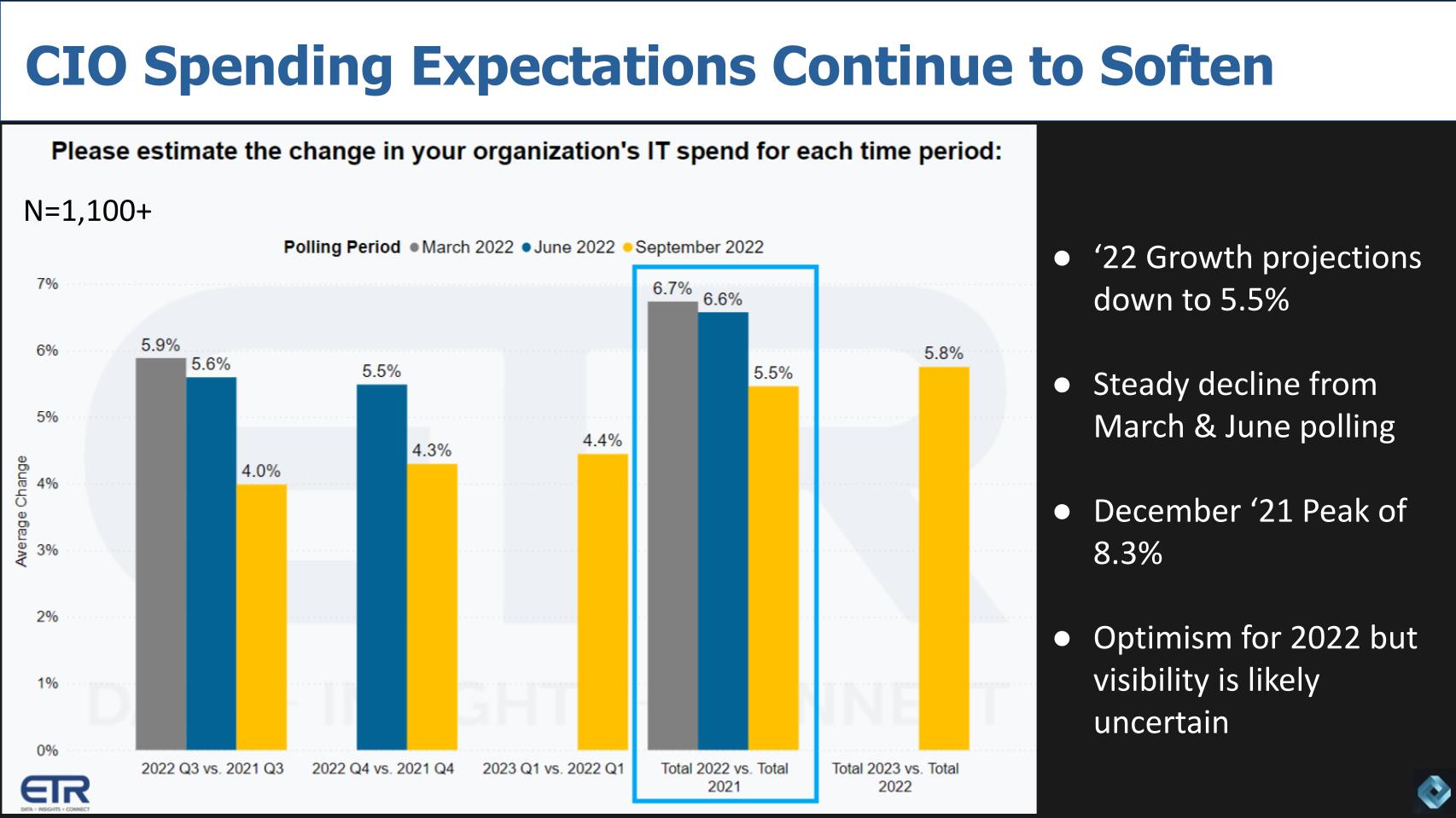

Steady Decline in Spending Expectations…But Ahead of Historical Norms

CIO’s were much more optimistic at the end of last year than they are today. Back then they thought their aggregate spend would increase by more than 8%. The graphic below shows where they are today.

Of course at that time the expectation was the economy was ready to make a semi-ordered return to normal. That didn’t happen and as you see above, the forecast for spending this year is down to 5.5% growth. This is based on the most recent ETR CIO survey, which includes more than 1,100 respondents. We started the year above 8% then made a meaningful decline to the mid sixes and 9 months into the year we’re now at the mid 5% growth range.

This growth still represents 200 to 300 basis points above historical norms. And looking ahead to next year, CIOs are expecting accelerated growth edging back toward the 6% level. As noted, visibility is less clear than in pre-COVID years. But the bottom line is digital transformations are continuing to push IT spending above historical levels.

The problem as we know is earnings estimates are coming down and forecasts are being lowered every day. As the saying goes, the first disappointment is rarely the last. Even the semiconductor industry is seeing softness. Just this past week we saw AMD lower its quarterly revenue forecast by more than $1B as PC demand in the second half has significantly softened. But again – that’s relative to some pretty amazing growth years thanks to the isolation economy.

Just this past week we saw AMD lower its quarterly revenue forecast by more than $1B as PC demand in the second half has significantly softened.

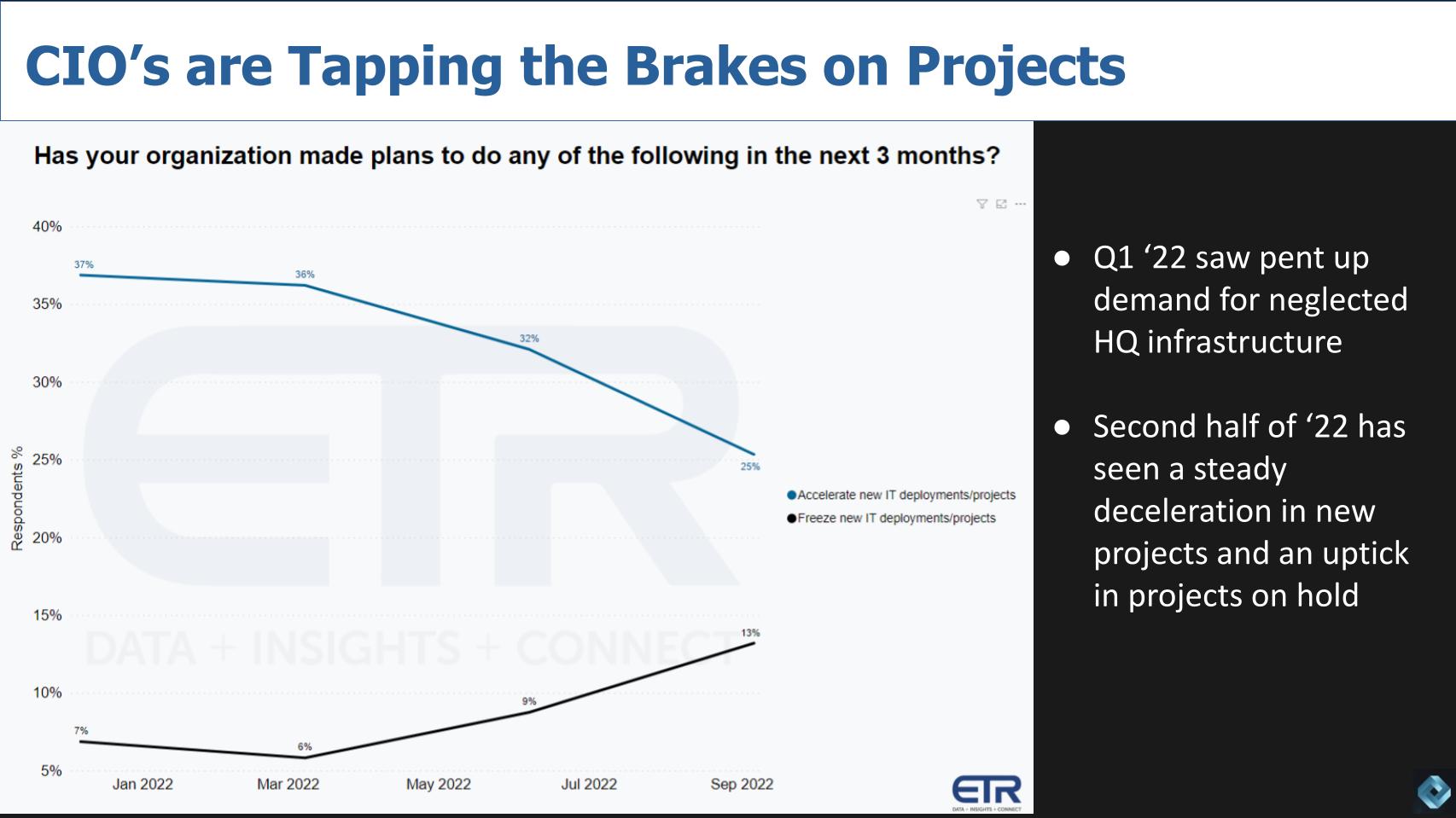

CIOs are Tapping the Brakes

We see CIOs slowing things down a bit and these data points below tell an interesting story.

ETR asked respondents about various actions they’re taking and these two stood out. The top line is “we’re accelerating new IT projects.” The bottom line is “we’re freezing projects.” You can see the convergence of those two lines which of course signals a slowdown.

But again these are not alarming data points. In Q1 2020, the top line was at 12% versus 25% today and project freezes were at 22% versus 13% today. Relatively speaking the spending dynamic is still strong.

In Q1 2020, the top line was at 12% versus 25% today and project freezes were at 22% versus 13% today. Relatively speaking the spending dynamic is still strong.

It just doesn’t feel that way because we’re coming out of an historic anomaly.

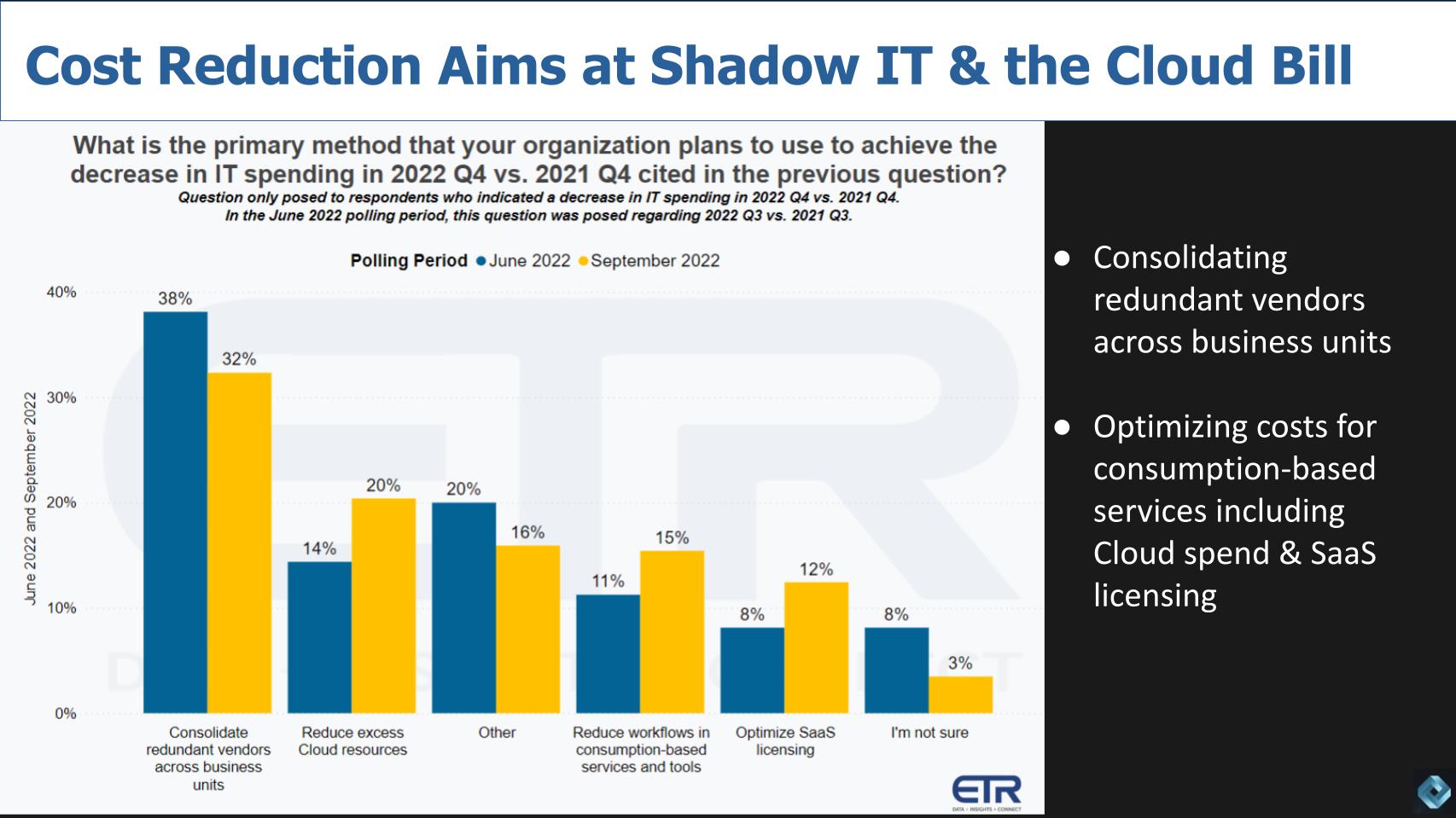

Vendor Consolidation & Dialing Down Consumption are the Common Cost Cutting Strategies

ETR asked a follow up question to only those respondents that indicated spending would be down this quarter relative to the same quarter last year. They wanted to better understand the most common actions that organizations would take to save money. That data is shown below.

The chart shows the most common approach is still to consolidate redundant vendors across the lines of business. So presumably, CIOs have the latitude to go after shadow projects and implement standards across the organization via consolidation.

As well, there was a big jump in this survey – from 14% to 20% – of respondents saying they were going after the cloud bill and that relates to the fourth set of bars which is scrutinizing consumption based services. So combined, 45% of respondents are looking at reducing their on-demand spend. Some of that may be SaaS-related but most of the SaaS spend is committed but we do see organizations doing more audits to eliminate or reduce orphaned licenses.

45% of respondents are looking at reducing their on-demand spend.

Cybersecurity Remains a Priority. Data-Related Initiatives See a Bounce

The last data point we want to focus on is the technology sectors that are of the highest priority. The top areas are shown below.

While cybersecurity remains the top technology area, even this sector is showing a little bit of softness. What’s really notable is the uptick in data-related areas – the second set of bars. This category is now the second most cited taking over from cloud, which remains strong and continues to be a key component of digital transformations.

As we’ve previously reported, the Machine Learning/AI and RPA sectors appear to be somewhat more strategic and discretionary. And they’ve dropped below the 40% mark in terms of Net Score in the overall survey. We’re not showing that here but we covered this in our last Breaking Analysis.

Now remember – these are the top 7 sectors – there are dozens in the ETR taxonomy so making this list is goodness from a spending perspective. So even though there’s some softness in most of these categories, these are the ones CIOs are most focused on addressing.

Takeaways from the Latest Spending Data

The messages in this data are:

- Spending targets are coming down to the mid 5% range but this is meaningfully higher than historical norms. While CIOs are pumping the brakes on projects, they’re still moving forward at rates faster than pre-COVID levels and freezing fewer projects. While a skills shortage could be in play here, we think the slowdown is likely more related to economic uncertainty;

- We’re seeing the two sided coin of “pay-by-the-drink” consumption models. You can dial it up as needed but you can also dial it down. That’s one of the alluring features of on-demand. And we’re seeing firms give more scrutiny to the cloud bill. And there’s a bit of an unsurprising backlash to the flaws in the SaaS pricing model that locks you in for specified terms;

- The real savings however are coming from eliminating redundant vendors, which could favor some of the larger firms like Microsoft, Amazon, Oracle, Dell, Salesforce, ServiceNow, IBM, HPE, Cisco and others;

- Having said that, we see an uptick in data-related areas as a priority for CIOs and that could mean companies like Snowflake are in a strong position to continue to thrive. Even though, as we reported last week, virtually all companies and sectors in the ETR data set are showing some softness related to spending momentum from previous quarters.

While it feels like a meaningful slowdown, the sky is by no means falling. There are these “out of our control” factors like interest rates, Ukraine, oil supply, wages, etc. that are creating uncertainty and causing firms to be more cautious.

But generally we remain optimistic as leading tech companies are well managed and have plenty of runway on the balance sheets. As such they can adjust costs to reflect the uncertain environment and remain flexible in doing so.

Keep in Touch

Thanks to Alex Myerson and Ken Shiffman are on production, podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight who help us keep our community informed and get the word out. And to Rob Hof, our EiC at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis