While we’ve been skeptical about repatriation as a notable movement, anecdotal evidence suggests that it is happening in certain pockets. Even though we still don’t see cloud repatriation broadly showing in the numbers, certain examples have caught our attention. In addition, the potential impact of AI raises some interesting questions about where infrastructure should be physically located and causes us to revisit our premise that repatriation is an isolated and negligible trend.

In this Breaking Analysis we look at a number of sources, including the experiences of 37signals, which has documented its departure from public clouds. We’ll also examine the relationship between repatriation and SRE Ops skill sets. As always we’ll look at survey data from our partners at ETR, a recent FinOps study published by Vega Cloud and revisit the Cloud Repatriation Index, which we believe is breaking a three-year trend.

Plenty Written on Cloud Repatriation

Many credible sources have published on the topic.

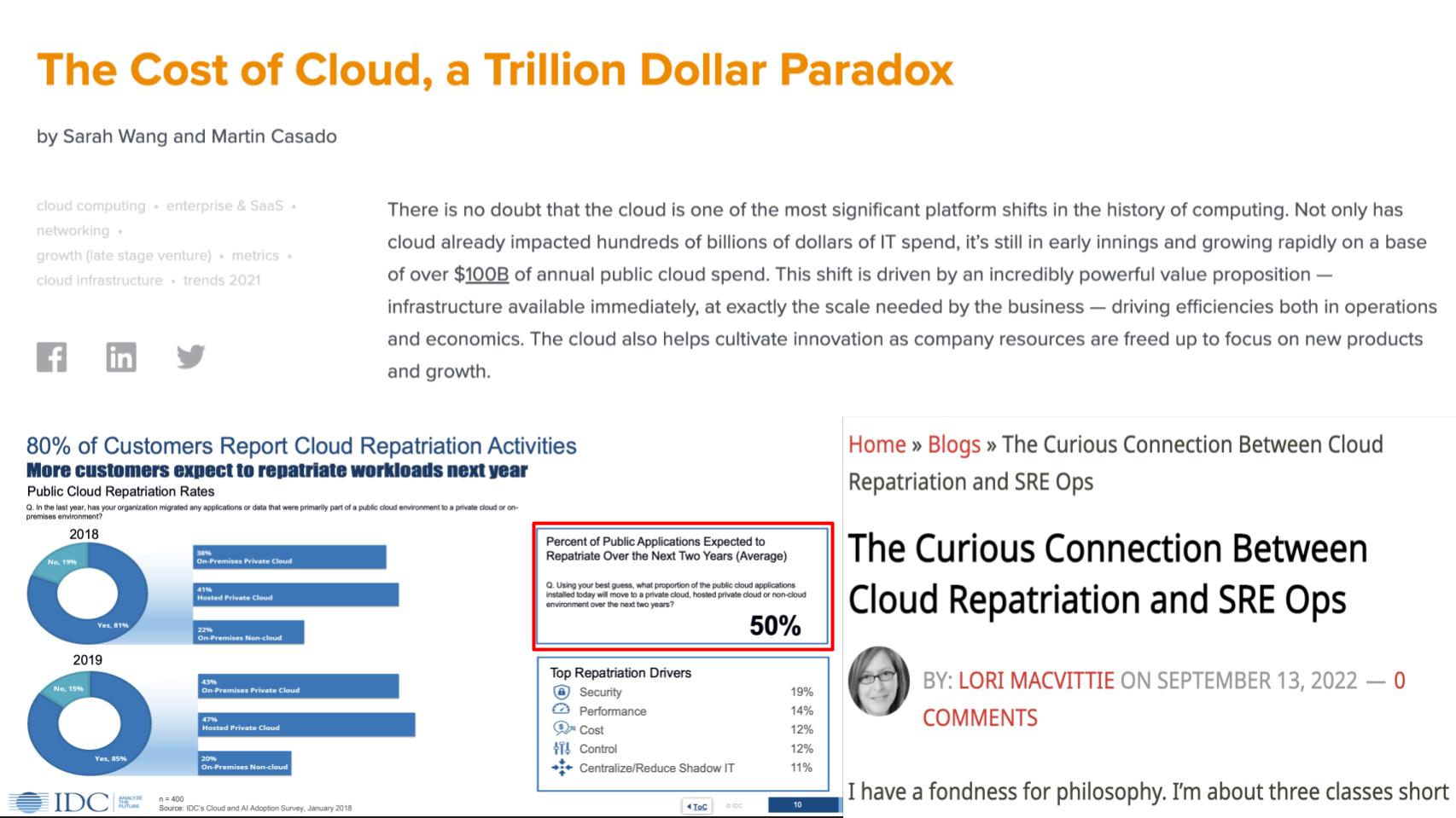

On the bottom left, IDC published a report in 2018 that said over the next two years users expected 50 percent of public cloud applications to repatriate. We found that to be an astoundingly large figure. This study was done by Michelle Bailey and Matt Eastwood, two highly respected and credible analysts. We know their work and from what we can tell this wasn’t a sponsored study.

The most discussed report continues to be the somewhat controversial but widely referenced work from Sarah Wang and Martin Casado of Andreesen Horowitz. The post posited that cloud expenses would become an increasingly large component of cost of goods sold (COGS) for cloud native SaaS companies at scale. And these costs would become so dilutive to profits that it would either force repatriation or a large discount concession from cloud providers. The authors used the Dropbox case study as an example of the potential savings from repatriation where the company saved $75M by moving infrastructure back on prem.

How (we think) Snowflake is Managing its Cloud COGS Conundrum

You’ll find some evidence of this COGS issue in Snowflake’s 10K. In the most recent March 2023 filing there’s the following note:

In January 2023, we amended one of our third-party cloud infrastructure agreements [presumably AWS] effective February 1, 2023. Under the amended agreement, we have committed to spend an aggregate of at least $2.5 billion from fiscal 2024 to fiscal 2028 on cloud infrastructure services.

And Snowflake is contractually obligated to pay any difference between the commitment and what they use during that term.

Sounds onerous right?

But as you read on, you’ll find this tidbit:

The remaining non-cancelable purchase commitments under the agreement prior to the January 2023 Amendment, the aggregate amount of which was $732.0 million as of January 31, 2023, is not reflected in the table above as the Company is no longer required to fulfill such commitments.

So two points here that we’ve made before and will reiterate.

- That last notation is an indication that Snowflake has re-negotiated its contract with AWS and retired $732M from its previous committed spend. Ostensibly to get a large discount. Thus far, the quid pro quo has been you buy more we’ll give you a break so you can manage cloud COGS. And this will likely continue indefinitely.

We see the same trend happening within the broader customer base where buyers are locking into longer terms with savings plans but committing to a specific spend amount.

- The second point relates to Dropbox. Dropbox is bad example of repatriation in our opinion because you cannot build a third party object storage service on top of S3 and make money. Ask David Friend, CEO of Wasabi or Gleb Budman the founder & CEO of Backblaze, two companies with object storage offerings. They will confirm this.

[Listen to Gleb Budman explain the economics of scale out cloud storage on the Cloudcast Podcast].

So while it might make sense to do some things on-prem such as what Zscaler or CrowdStrike as was reported by Wang and Casado, so far repatriation from SaaS companies like Datadog and Snowflake has not been a factor.

Game Over, Cloud Wins…(Wait not so fast)

Let’s not call final victory for cloud just yet. Lori MacVittie put out an interesting post late last year describing the relationship between site reliability engineering (SRE) skills and cloud repatriation. Her point was not that SRE causes repatriation, rather that SRE skills make it easier for companies to operate on-prem infrastructure using a cloud operating model. She cited an F5 report that showed a significant jump from 2021 to 2022 in customers repatriating apps. And she asked the right question…i.e.

It’s not whether repatriation happens, we know it does…the question is what percentage of workloads are actually moving back?

It doesn’t appear to be 50% based on the data we have but her point is that many more customers today have SRE Ops capabilities and are in a better position to repatriate…if there’s a business case.

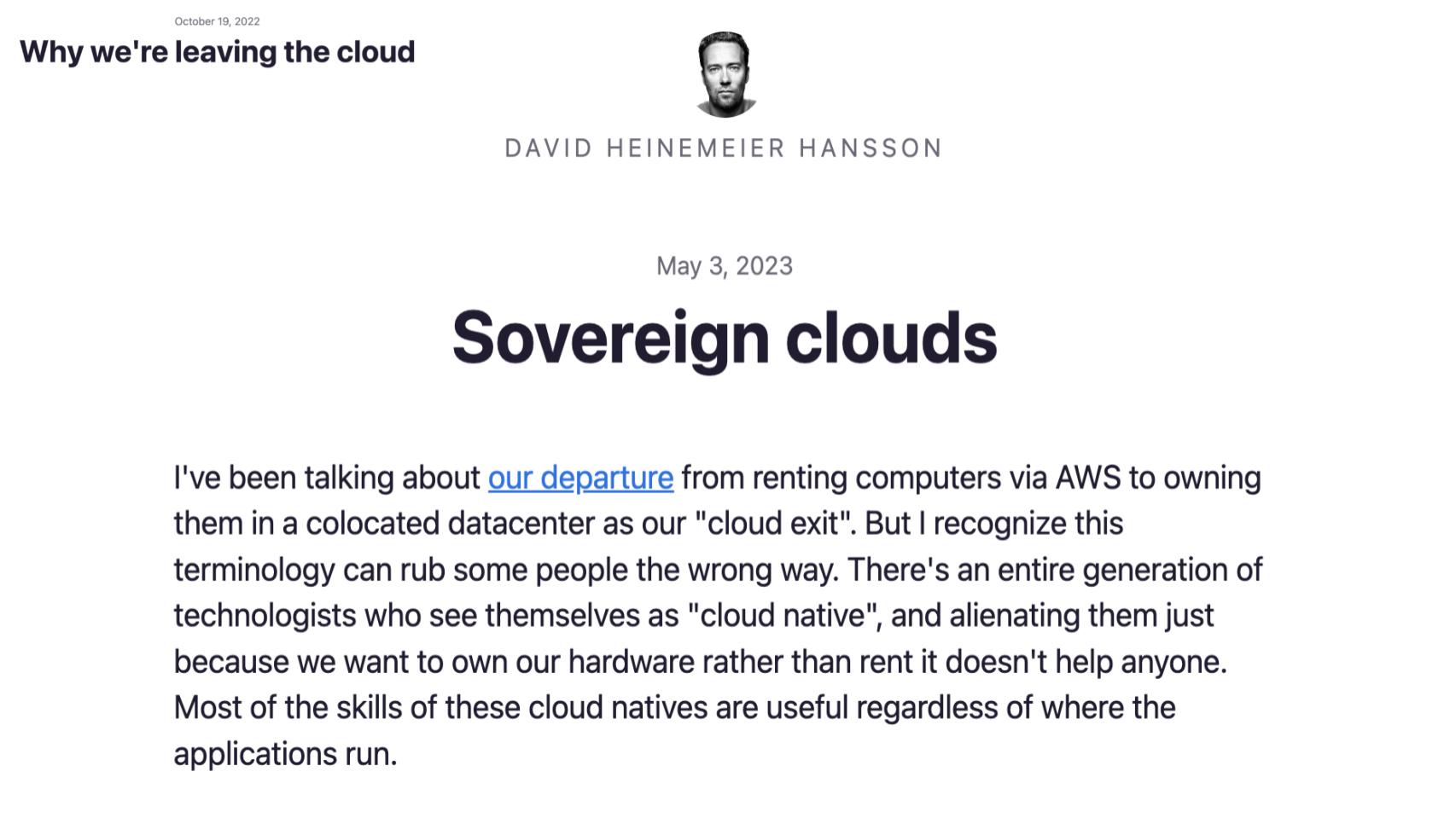

The 37signals Sovereign Cloud Story

Which brings us to the 37signals repatriation case study.

David Heinemeier Hansson is the co-founder of 37signals, a much admired software company with popular products like Basecamp and Hay. He’s published a couple of posts on the company’s departure from cloud and he used this term sovereign cloud, as an alternative to private cloud or on-prem. VMware has used this term for years as has CUBE analyst and colleague David Nicholson. The implication is cross cloud and hybrid services are emerging that will require control planes which live outside of a limited number of public clouds. Moreover, according to Nicholson, at the end of the day “it’s all IT” implying that the off prem and on-prem worlds are converging and reaching a state of quasi-equilibrium.

David Heinemeier Hansson is the co-founder of 37signals, a much admired software company with popular products like Basecamp and Hay. He’s published a couple of posts on the company’s departure from cloud and he used this term sovereign cloud, as an alternative to private cloud or on-prem. VMware has used this term for years as has CUBE analyst and colleague David Nicholson. The implication is cross cloud and hybrid services are emerging that will require control planes which live outside of a limited number of public clouds. Moreover, according to Nicholson, at the end of the day “it’s all IT” implying that the off prem and on-prem worlds are converging and reaching a state of quasi-equilibrium.

[Listen to VMware’s Chris Wolf give his perspective on so-called sovereign cloud].

Remember, 37signals are well known iconoclasts and anti-establishment types. But their economic argument is nonetheless sound. Specifically that renting infrastructure for a mid-sized firm like 37signals is more expensive today than when they were starting out with new products in the cloud. The other key point aligns with Lori MacVittie’s premise that the skills overlap between what it takes to run software in the cloud versus on-prem is 80-90% correlated. With some differences of course. Such as:

- You don’t need FinOps and forensic accounting to understand your cloud bills

- You have to maintain equipment, patch servers, worry about physical security, replace failed hardware, etc.

Heinemeier Hansson claims these differences are minor and easier than learning Kubernetes.

Maybe so. But many, or most mid-sized companies don’t have the developer talent of 37signals and would rather invest elsewhere.

Back to the Future

Below is a picture of the 37signals sovereign cloud.

Look at those lovely shrink wrapped boxes on a wooden pallet! You can see the infrastructure they bought on the right. 37signals are geeking out and having fun with hardware. Check out the Dell R7625s with two AMD EPYC 9454 CPUs running at 2.75GHz with 48 cores / 96 thread. According to 37signals, this adds 4,000 vCPUs to their on-premise fleet. With 7TBs of RAM and 384TB of Gen 4 NVMe storage, moving to Gen 5 they’ll get to ~13GB/sec soon.

Yeah so cool. Sovereign cloud. Go for it if you have the chops.

How Widespread is this Trend?

Let’s take a look at the data and see if there’s any evidence of repatriation.

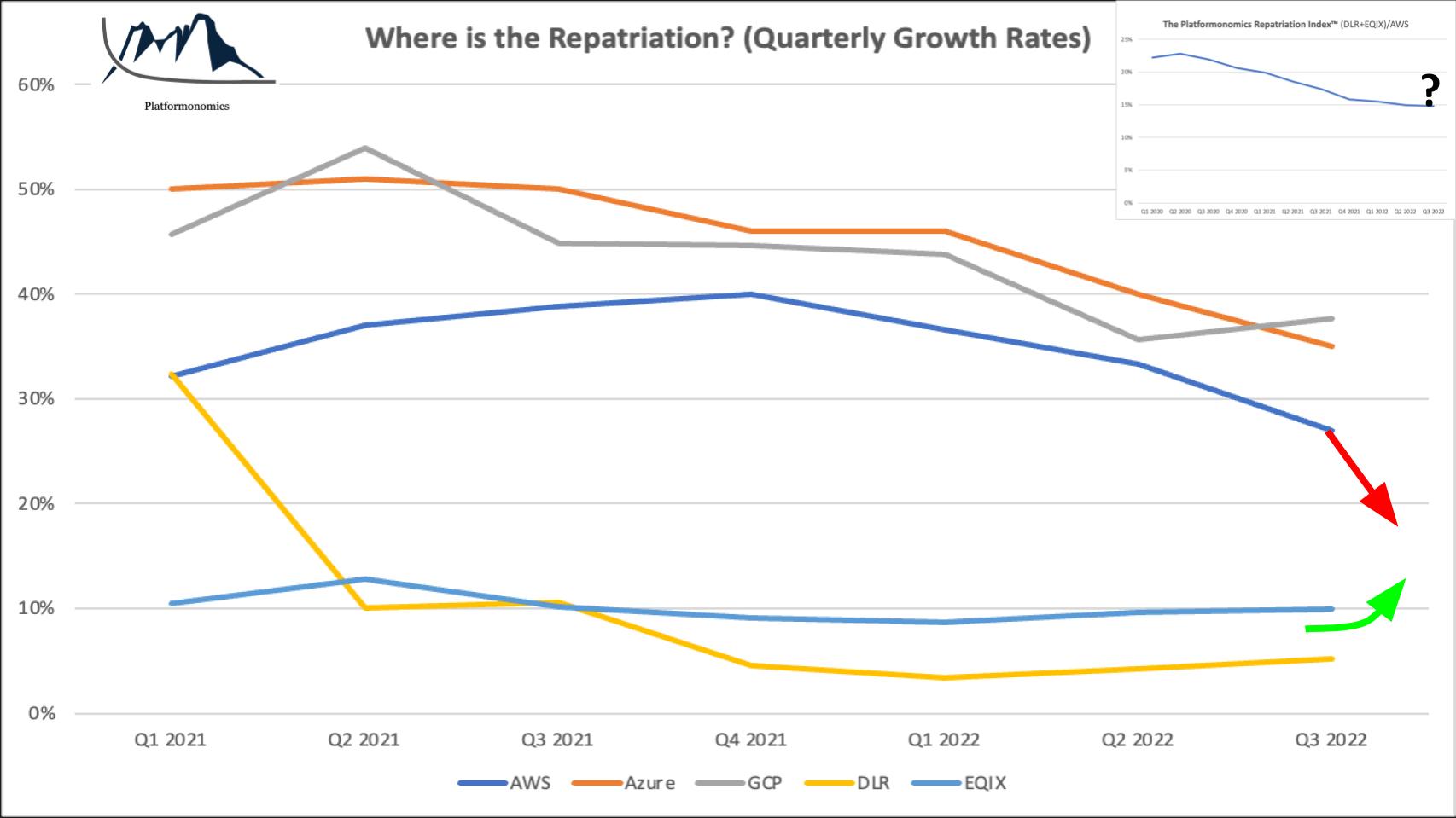

Our friend over at Platformonomics, Charles Fitgzerald created what he calls the Cloud Repatriation Index.

In the chart above he plots the growth rates of the big three cloud players against those of Equinix and Digital Realty. And in the upper right we show Fitzy’s repatriation index which takes the revenue of the two leading colos and divides by AWS’ cloud revenue. That blue line in the upper right has been on a steady downward trend for three years. But you’ll notice in the chart below, the growth rates based on 2023 projections are converging…so that flattening repatriation curve is likely upticking the way it was back in early 2020.

We’ll keep an eye on that because both big colocation players are forecasting strong revenue growth. Equinix’ guide is for 14-15% revenue growth, which could exceed AWS’ growth rate. Digital Realty is expected to grow revenues slightly below Equinix but in the low teens, so combined they’re converging with the growth rates of AWS.

So based on the likely next rev of Charles’ repatriation math, we’re likely to see some convergence.

No Overwhelming Evidence in Customer Surveys

Let’s bring in some ETR survey data and take a look at whether there are signs that repatriation is happening to a large degree.

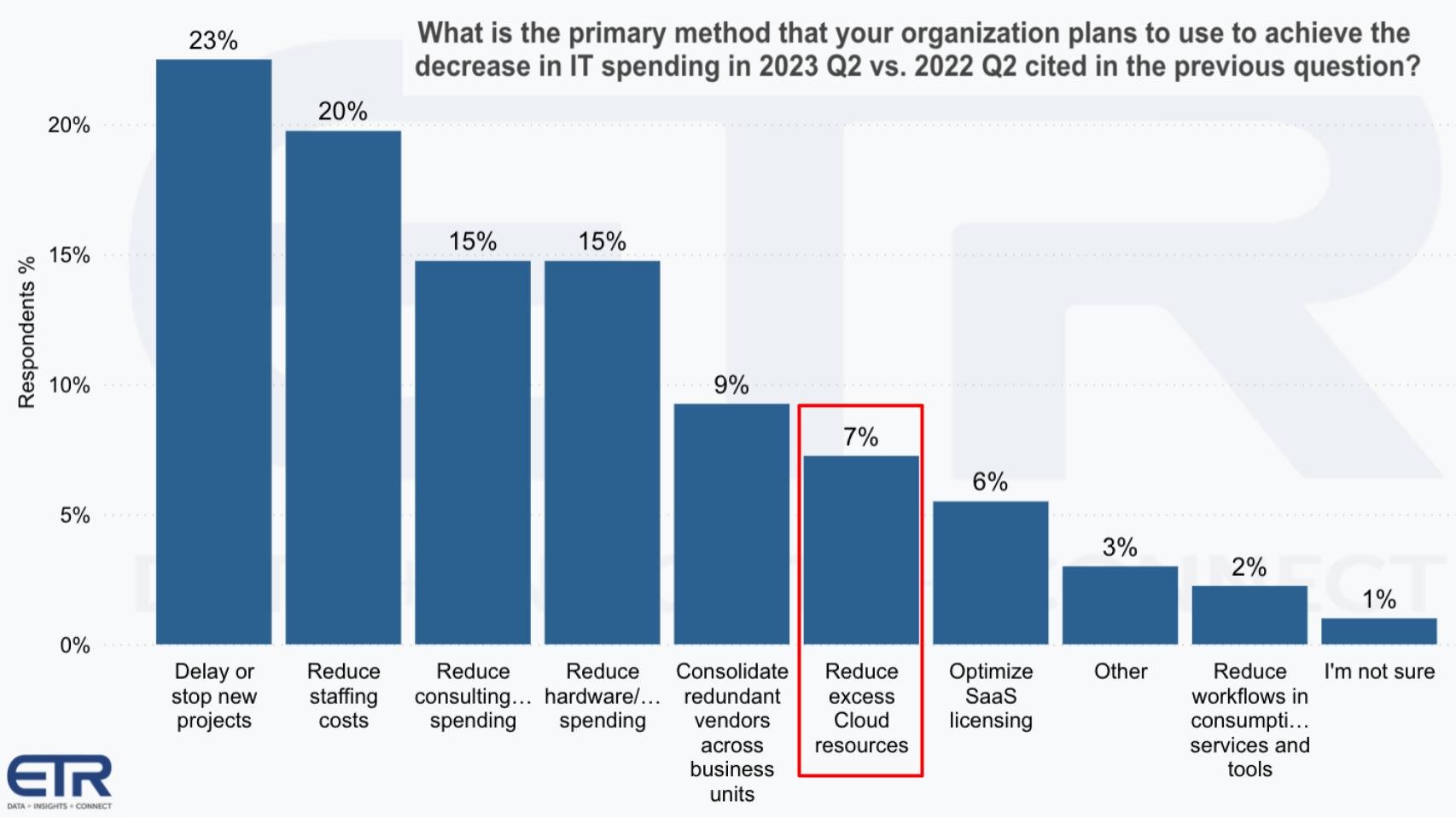

In this recent drilldown, ETR asked 400 respondents that said they were significantly cutting costs how they were doing so. And you can see above they’re delaying projects, cutting staff, reducing consulting spend, holding off on hardware purchases, consolidating redundant vendors – by the way that was #1 last quarter… and finally, reducing excess cloud resources.

Reducing excess cloud resources might include some repatriation. We asked ETR to look into this and dig into the open ended comments and repatriation didn’t come up specifically. But that doesn’t mean it’s not happening in pockets. It just doesn’t appear to be “thing 1” as Stu Miniman likes to say.

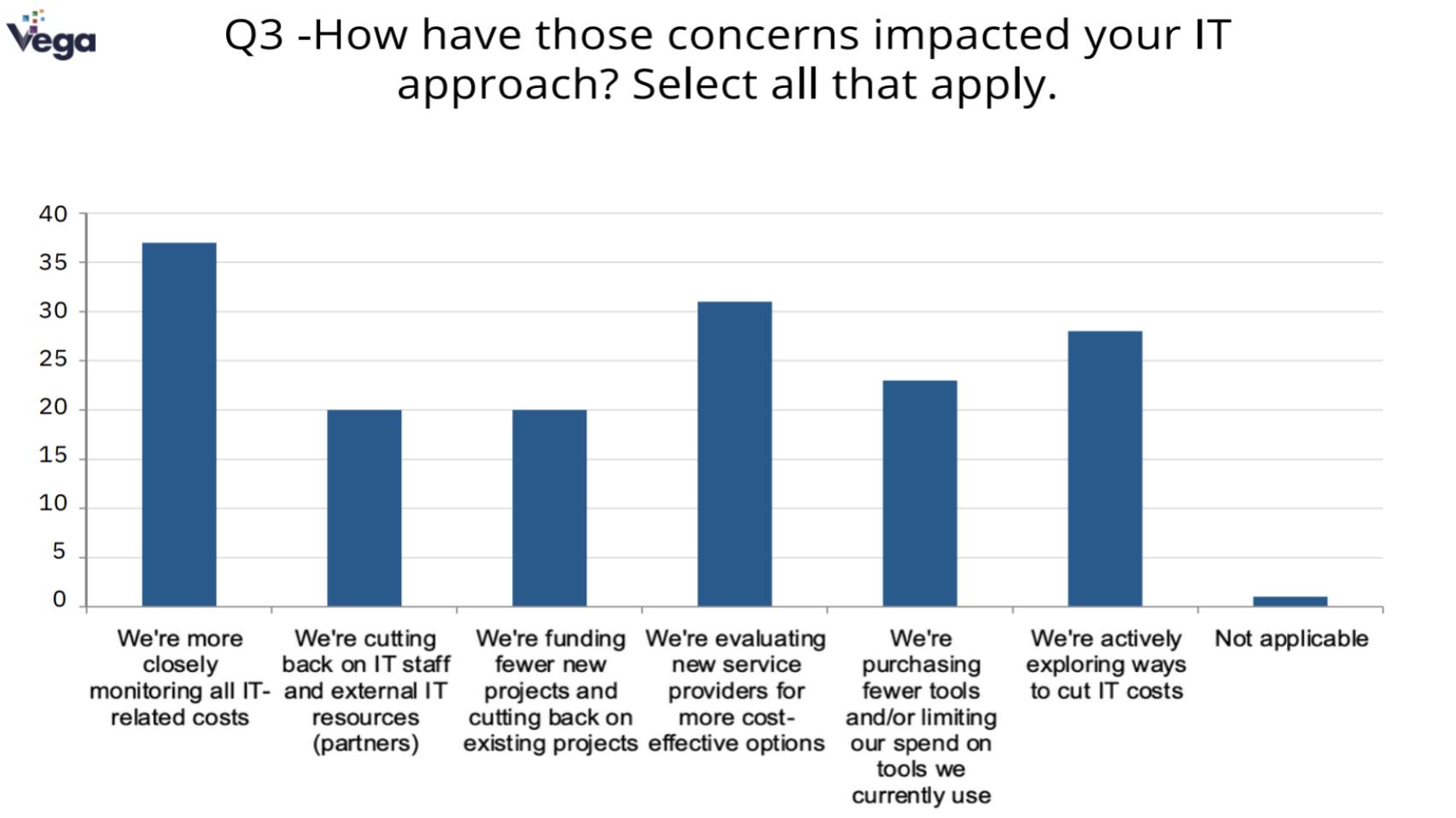

Vega Cloud FinOps Survey

We recently received an inbound from Vega Cloud, a firm specializing in cutting cloud costs. And they just ran a survey on FinOps. The chart below shows, actions taken by customers concerned about cloud costs.

Somewhat consistent with the ETR data we see staff cuts, project delays, vendor alternatives, etc. but no specific evidence of repatriation.

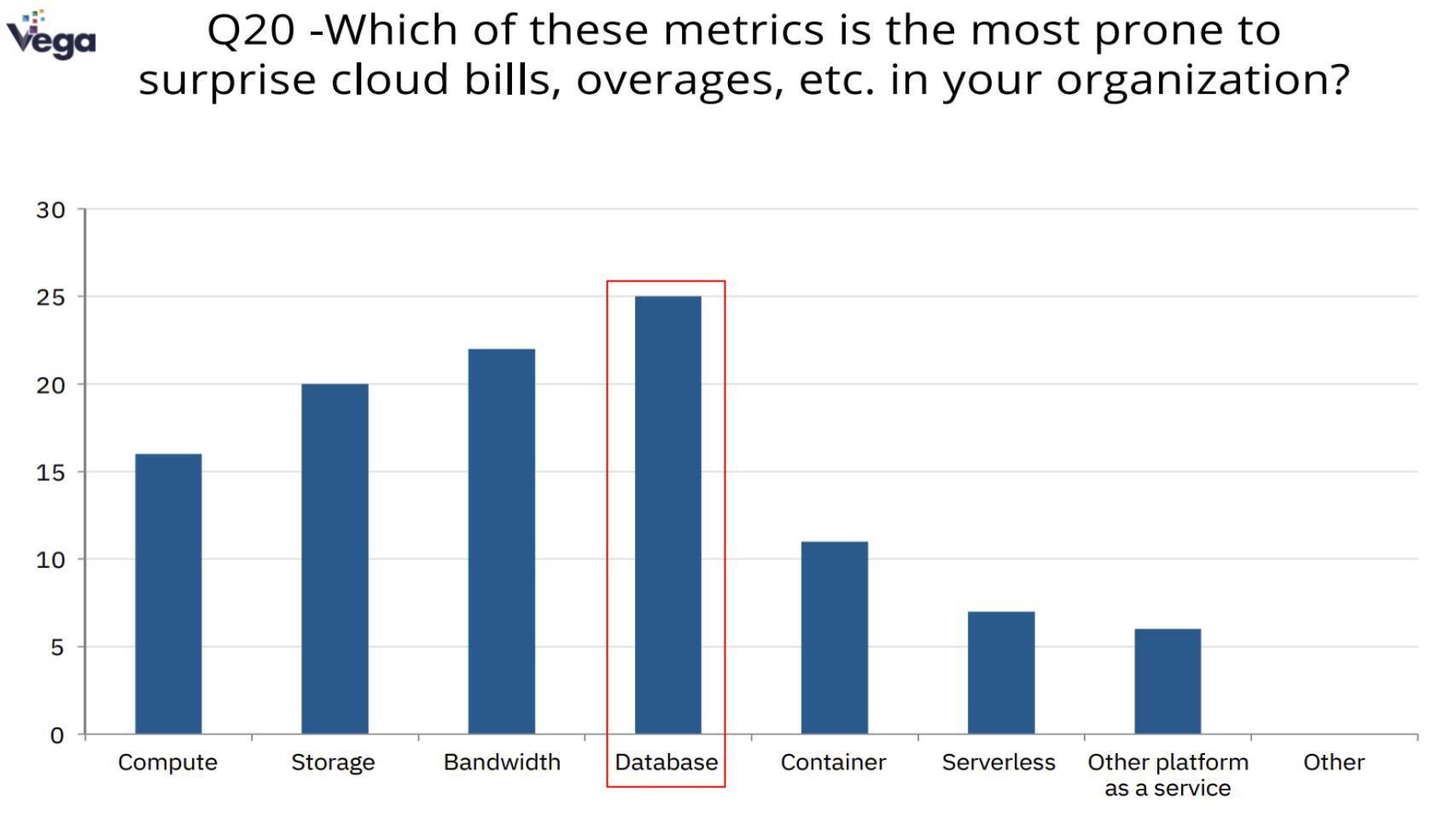

Database is the Biggest Surprise in Cloud Cost Overages

One notable callout in the Vega survey was a question about which line items on the cloud bill were giving them the most heartburn from overages relative to expectations.

We would have thought compute and bandwidth would be the big culprits but database was number one. We wonder how many Snowflake customers were in this sample because Snowflake is a very popular database. And our understanding is it charges customers for consumption as a bundle. So the Snowflake customer doesn’t see granularity of storage or compute…just a Snowflake consumption bill. We asked the folks who did the survey but they don’t have that level of detail.

Repatriation or Not…Hybrid is the Dominant Model

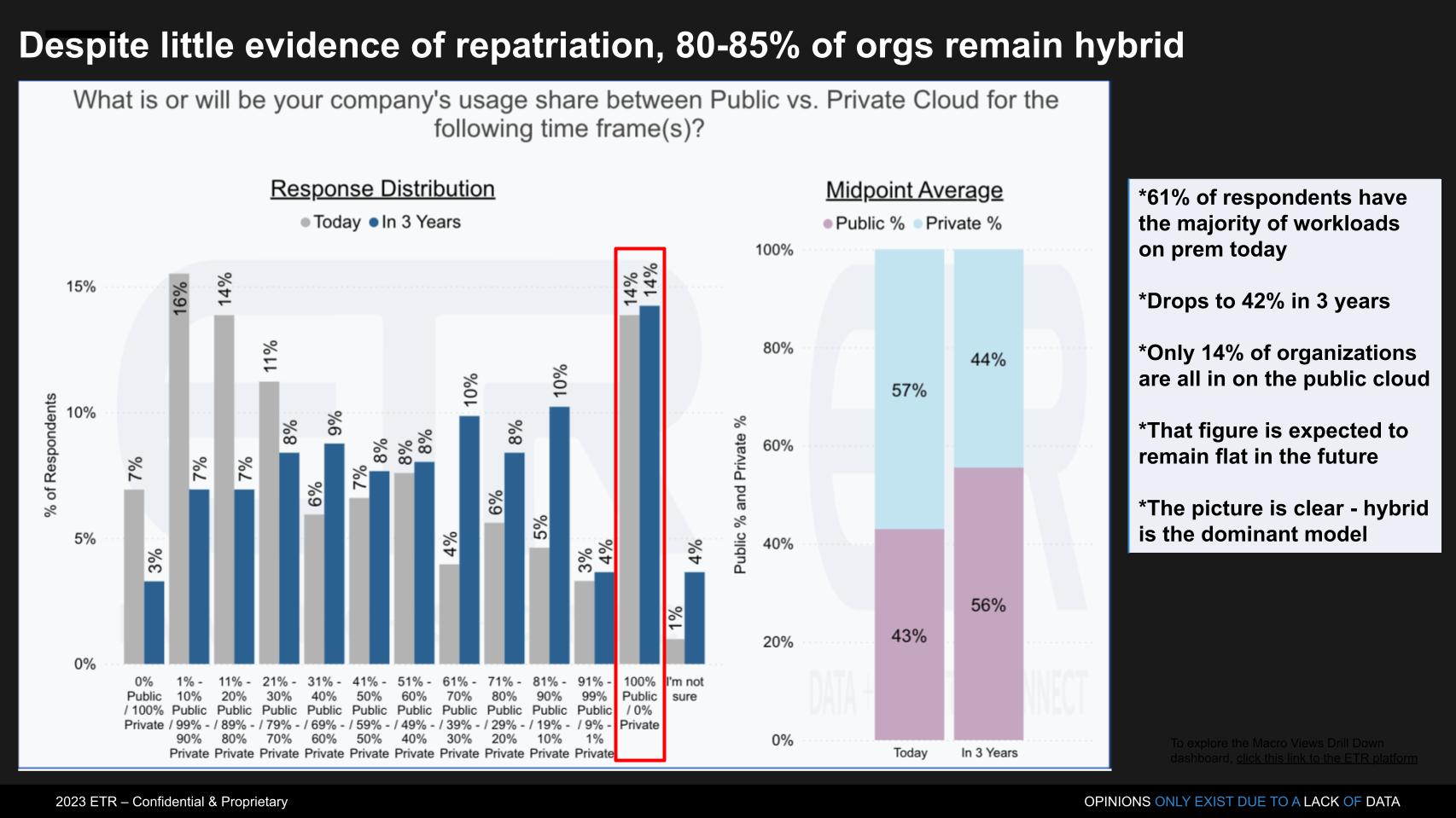

The last bit of ETR data we’ll look at is from a survey on cloud adoption relative to on-prem. And the preponderance of hybrid cloud.

We’ve shared the data above before but will take a different angle today. It’s from another ETR drilldown late last year which breaks down the percent usage between public and private cloud. The key points are:

- 61% of respondents cite the majority of their usage is on prem today. So that means 40% have most of their work being done in the cloud, which makes you question the claim that 90% of all workloads are on-prem today;

- The 61% figure drops to 42% in two years;

- But the real call out stat to us was that only 14% of customers say they’re all in on the public cloud and that is expected to remain flat over the next two years.

So first, if there’s repatriation happening at a large scale it’s not clear form these numbers. The second point is the picture is crystal clear…hybrid is the dominant model for the foreseeable future.

How will AI Impact Infrastructure Choices?

The other question we pondered is how will AI impact this picture.

First of all, foundation models like GPT are a tide that will lift all compute and infrastructure boats in our opinion. Automation combined with massive compute and data requirements will enable / require greater spending on servers, storage and networking.

As an example, it was interesting to see the stock market’s tepid reaction to AMD’s quarter this past week. The company beat estimates despite the challenging environment and soft PC market. And the stock dropped. But when it was announced that Microsoft is helping finance AI chips for AMD, its stock popped. And while a lot of that is hype around ChatGPT, it’s also recognition that we’re entering a new era where AI is going to drive massive demand for data center hardware.

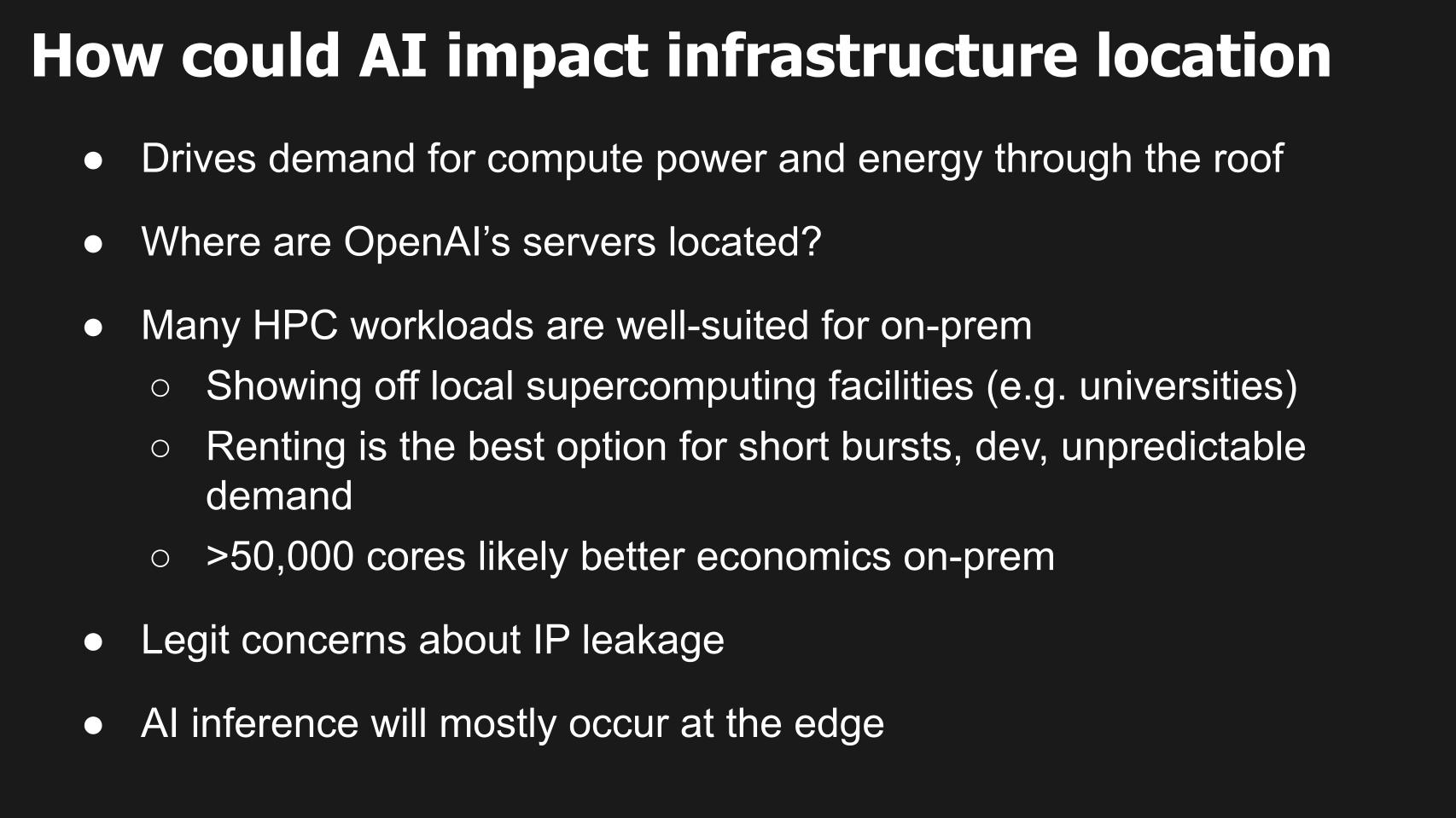

Which begs the question – where’s that hardware going to live? In the cloud or on-prem? Where are OpenAI’s servers? Well we know they’re in Azure but they’re evidently also in Ohio on a supercomputer where the training is done. We asked ChatGPT and got a vague answer but when you look at AI, there’s clearly an affinity between it and high performance computing.

And many of those HPC workloads will land on-prem. For example, if you’re a university and have a supercomputing center, you’ll want to show that off to prospective students and donors, versus having resources hidden away in a remote cloud. Renting infrastructure is economically viable for bursty use and unpredictable swings in demand but like the cloud v. on prem argument for mainstream apps, similar arguments apply in HPC. Especially with large scale implementations – e.g. more than 50,000 cores. Some supercomputers have millions of cores.

There are also legitimate concerns about leaking IP. We recently saw Samsung Electronics and other organizations ban ChatGPT after an employee put proprietary code into the software, not realizing the risks. Which makes AWS’ announcement of Bedrock interesting. AWS is not building a free service like Google Search or Bing or OpenAI…rather it’s offering large language model services and tools so you can build your own. Presumably making IP leakage less likely.

But then of course there’s Alexa.

And the last point is, as Matt Baker said on our LinkedIn post last week:

This is batting practice for AI, the game will be played at the edge and in the world around us. Adaptation and inferencing do not favor centralized models, e.g.public cloud.

We agree. AI inferencing is going to explode at the edge. Not in today’s public cloud. Now how the public cloud players approach this will be interesting with autonomous vehicles, robots, satellites and other edge infrastructure.

So yes we’re smacking GPT balls out of the park before the first inning has even started.

Let the games begin and we’ll see what happens.

Keep in Touch

Many thanks to Alex Myerson and Ken Shifman on production, podcasts and media workflows for Breaking Analysis. Special thanks to Kristen Martin and Cheryl Knight who help us keep our community informed and get the word out. And to Rob Hof, our EiC at SiliconANGLE.

Remember we publish each week on Wikibon and SiliconANGLE. These episodes are all available as podcasts wherever you listen.

Email david.vellante@siliconangle.com | DM @dvellante on Twitter | Comment on our LinkedIn posts.

Also, check out this ETR Tutorial we created, which explains the spending methodology in more detail.

Watch the full video analysis:

Image: Masson

Note: ETR is a separate company from Wikibon and SiliconANGLE. If you would like to cite or republish any of the company’s data, or inquire about its services, please contact ETR at legal@etr.ai.

All statements made regarding companies or securities are strictly beliefs, points of view and opinions held by SiliconANGLE Media, Enterprise Technology Research, other guests on theCUBE and guest writers. Such statements are not recommendations by these individuals to buy, sell or hold any security. The content presented does not constitute investment advice and should not be used as the basis for any investment decision. You and only you are responsible for your investment decisions.

Disclosure: Many of the companies cited in Breaking Analysis are sponsors of theCUBE and/or clients of Wikibon. None of these firms or other companies have any editorial control over or advanced viewing of what’s published in Breaking Analysis.